HMRC’s IR35 CEST Tool

IR35 is tax legislation imposed by HMRC to ensure tax compliance within a flexible workforce. Most of you reading this probably know what IR35 is – if not, read our easy IR35 guide.

HMRC CEST Tool – Determining your IR35 Status

As of April 2021, the end-hirer is responsible for determining your IR35 status. Despite that, it’s a good idea to understand how your status is determined.

HMRC has introduced an online tool called Check Employment Status for Tax (CEST) to assist you in determining your employment status. The IR35 CEST Tool is an intuitive and easy-to-use interface that guides you through a series of questions related to various aspects of your employment contract.

Is IR35 CEST Tool valid for determining your IR35 status?

The use of the IR35 CEST Tool developed by HMRC can be used to determine your IR35 status for tax purposes. However, it’s important to note that the CEST tool does not provide you with a binding determination that you can use at a tribunal. The purpose of the tool is to give you an idea of your status through a series of questions about your contract, which include:

- Contract details

- Worker responsibilities

- Work location, hours and task delegation

- Payment terms

- Benefits received

- Expense risks

This guide can help you navigate the HMRC CEST tool by explaining the purpose of some of the questions.

Please note, that this guide is not a substitute for professional advice. If you feel uncertain about the IR35 CEST Tool and prefer a more in-depth analysis of your working arrangement, you can seek professional advice to determine your IR35 status.

Payroll management company like Cool Company helps contractors maintain compliance with HMRC by taking care of everything from taxes to employment protection. When you use Cool Company’s services you automatically place yourself “inside” IR35 and are free from any IR35 compliance concerns.

Getting started with the HMRC CEST Tool

Using the HMRC CEST tool is easy. All you have to do is go to the site and answer the questions. There’s no requirement to register an email address to take the test or receive the results.

Ready to get started? Here are the 28 questions currently used by the CEST tool, followed by brief explanations:

Question 1: What do you want to find out?

The purpose of this first question is to help you clarify the goal of your inquiry. Possible answers are:

(a) If the off-payroll working rules (IR35) apply to a contract

(b) If some work is classed as employment or self-employment for tax purposes.

Contractors who want to know their IR35 status should choose (a).

Question 2: Who are you?

There are three selections here:

(a) Worker

(b) Hirer

(c) Agency

Question 3: What do you want to do?

This answer gives you two options:

(a) Make a determination, or

(b) Check a determination.

If you are looking to gain some clarification on your contract status, then choose (a).

Question 4: Do you provide your services through a limited company, partnership or unincorporated association?

Most contractors affected by IR35 operate through a limited liability company.

In contrast, an “unincorporated association” is created for a nonprofit group like an NGO or volunteer organization.

Choose “Yes” to proceed (if either of these scenarios apply to you).

Question 5: Have you already started working for this client?

There are two possible answers: (a) Yes

(b) No

Choose the appropriate answer to proceed.

Question 6: Will you be an “Office Holder”?

An Office Holder is a board member, company secretary, treasurer, trustee, or company director. Answering “Yes” suggests that you have a permanent, long-term relationship with the company.

Question 7: Have you ever sent a substitute to do this work?

There are three possible answers here:

(a) Yes, your client accepted them

(b) Yes, but your client did not accept them

(c) No, it has not happened

This is a critical question because contractors are usually hired to fulfill obligations that an end-hirer cannot cover with existing staff. If you send substitutes to do the work in your place, it sends a signal to HMRC that you are acting independently.

Question 8: Did you pay your substitute?

HMRC would like to know if you pay your substitutes. Answering “yes” to this question indicates further that you have a working arrangement with that person that is entirely independent of the end-hirer.

Question 9: Does your client have the right to move you from the task you originally agreed to do?

There are three possible answers here:

(a) Yes

(b) No, you would have to agree

(c) No, that would require a new contract or formal working arrangement

This is an essential question because contractors are usually hired for specific skills and often work on a project-by-project basis. This is in contrast to permanent employees whose roles can change depending on the needs of the organization.

Question 10: Does your client have the right to decide how the work is done?

This is another general question that attempts to determine the nature of your role in the company. Many permanent employees work under the guidance of a manager, while contractors are typically hired on a temporary basis for their specialised skills.

It logically follows that if a contractor is hired to fill a void, then a manager should not be giving them directions on how to do their job.

Question 11: Does your client have the right to decide your working hours?

Most contractors work on deadlines, while permanent employees typically work on a set schedule. There are four possible answers to this question that offer flexibility for certain situations:

(a) Yes

(b) No, you solely decide

(c) No, you and your client agree

(d)No, the work is based on agreed deadlines

For the purposes of IR35, (a) is the answer that points most directly to an employer-employee relationship.

Question 12: Does your client have the right to decide where you do the work?

There are four answers here that allow for some flexibility that include:

(a) Yes

(b) No, you solely decide

(c) No, the task sets the location

(d) No, some work has to be done in an agreed location and some can be your choice.

Question 13: Will you have to buy equipment before your client pays you?

This question attempts to determine your level of risk. HMRC considers heavy machinery or high-cost specialist equipment to be “equipment” and excludes laptops, tablets and phones. If a contractor buys this equipment prior to being paid, it further indicates an independent relationship.

Question 14: Will you have to fund any vehicle costs before your client pays you?

This question is of a similar nature to Question 13, and a “Yes” answer indicates the contractor operates independently.

Question 15: Will you have to buy materials before your client pays you?

“Materials” according to HMRC can include items that form a lasting part of the work or are left behind after completion, such as construction materials. Like the previous two questions, answering “Yes” indicates a higher level of risk and independence.

Question 16: Will you have to fund any other costs before your client pays you?

This question is similar to Questions 12-14 and includes any materials, equipment or costs such as non-commuting travel, accommodation, or external location costs connected to the contract.

Question 17: How will you be paid for this work?

This is a critical question because the method of payment provides disclosure into the nature of the relationship. There are four possible answers here:

(a) An hourly, daily or weekly rate

(b) A fixed price for the project

(c) A fixed amount for each piece of work completed

(d) A percentage of the sales you generate

(e) A percentage of your client’s profits or savings

Some methods of payment indicate more independence, while others indicate close ties to the end-hirer, such as (d) and (e).

Question 18: If the client was not happy with your work, would you have to put it right?

It might be argued that this is a trick question, however the main idea here is that permanent employees typically do not get paid extra if they make mistakes. There are several answers that provide flexibility that may include:

(a) Yes, unpaid and you would have extra costs that your client would not pay for

(b) Yes, unpaid but your only cost would be losing the opportunity to do other work

(c) Yes, you would fix it in your usual hours at your usual rate or fee

(d) No, the work is time-specific or for a single event

(e) No

Question 19: Will your client provide you with paid-for corporate benefits?

This critical question provides disclosure into the nature of your relationship with the end-hirer. Unlike permanent employees, contractors typically don’t receive employee-only perks like party invites, gym memberships, health insurance or retail discounts.

Question 20: Will you have any management responsibilities for your client?

HMRC defines “management responsibilities” as “deciding how much to pay someone, hiring or dismissing workers, and delivering appraisals”. These types of duties indicate a permanent nature to the job and are typically not handled by outside contractors.

Question 21: How would you introduce yourself to your client’s consumers or suppliers?

Do contractors typically engage with a client’s customers and vendors? The answer in most cases is “sometimes” – however, the difference lies in how the contractor is represented. There are four choices to answer this question that include:

(a) You work for your client

(b) You are an independent worker acting on your client’s behalf

(c) You work for your own business

(d) This would not happen

Question 22: Does this contract stop you from doing similar work for other clients?

If a contractor works exclusively for one client, this typically indicates an exclusive arrangement in the eyes of HMRC.

Question 23: Are you required to ask permission to work for other clients?

Similar to the previous question, your answer here helps HMRC determine the exclusivity of your arrangement with the end-hirer.

Question 24: Are there any ownership rights relating to this contract?

Many contracts in media, arts and other creative industries include intellectual property rights, copyright, trademarks, patents, and image rights. Unlike a permanent employee, a contractor that operates independently may have the option to maintain those rights.

Question 25: Have you had a previous contract with this client?

This question helps HMRC determine the length of your relationship. If it includes multiple contracts without breaks, this may indicate a permanent relationship with the end-hirer.

Question 26: Is the current contract the first in a series of contracts agreed with this client?

This question is in line with the previous question. Multiple back-to-back contracts typically indicate a permanent relationship.

Question 27: Will this work take up the majority of your available working time?

The answer to this question typically gives insight into the time and effort commitment you have to this client, and a “Yes” response may indicate a long-term relationship.

Question 28: Have you done any self-employed work of a similar nature for other clients in the last 12 months?

This question basically builds on the last question, seeking to determine the exclusivity of your relationship with the client.

Review the answers in the HMRC CEST tool

After you have answered the questions in the CEST tool, you will be asked to review your answers. After confirming your responses, you will be given the results.

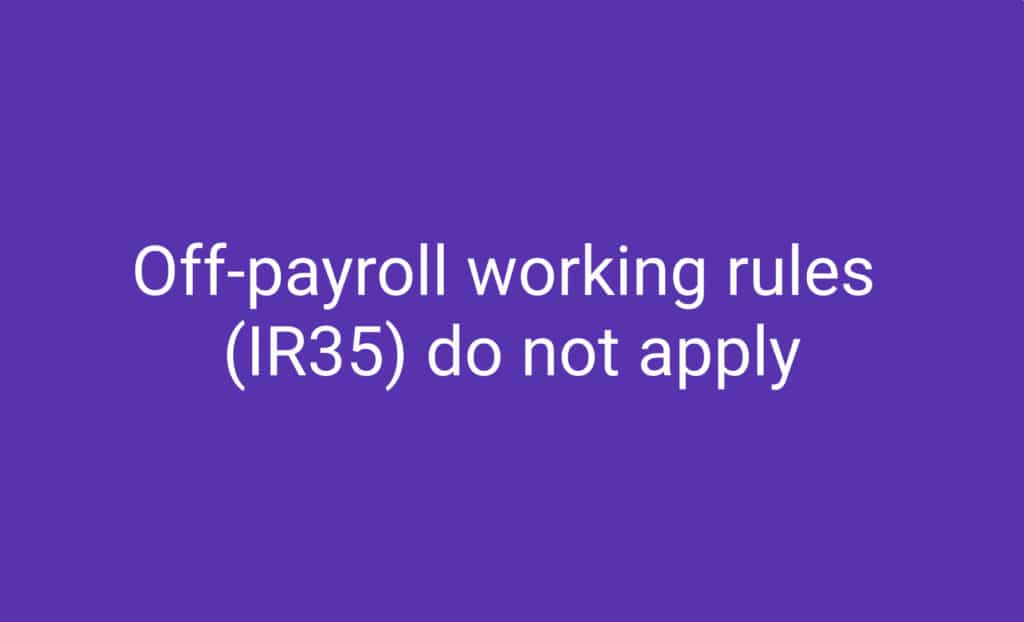

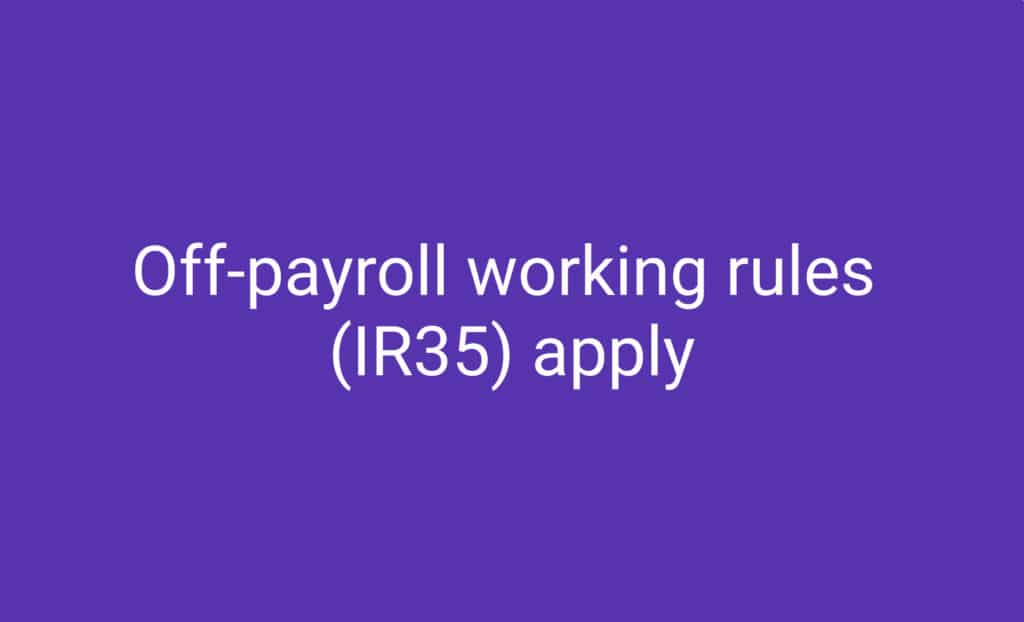

Some of you will get this:

And some of you will get this:

Determining your IR35 status can be complex

Even with the help of IR35 CEST tool, determining your IR35 status can be difficult, and for many individuals, it may fall into a grey area where it’s unclear whether they are inside or outside of IR35.

If you’d prefer to avoid dealing with the complexities of IR35 and focus on your work, why not let a payroll company like Cool Company handle it for you? We take care of everything, including taxes, insurance, employment protection, and more.

Our intuitive, easy-to-use interface allows you to track your clients and assignments. All you have to do is submit your timesheet and get paid. How easy is that?